Photo and notes provided by the user — not generated by AI

Submitted photo · July 11, 2026

User's notes

Good condition

AI analysis below

AI appraisal

AI analysis & estimate

AI-Generated · Verify before acting

Everything below is generated by AI for informational purposes only. AI can make mistakes — the AI may misidentify items or misattribute them (artist, maker, brand, designer, origin, era). This is not an official valuation and should not be used for insurance, sale, tax, estate, legal, or lending purposes — or any decision requiring a certified appraisal. It is not an authoritative claim about any person, brand, or rights holder — do not share or rely on it as a factual statement about a third party. Always consult qualified professionals before making financial decisions.

Note

This analysis also relies on unverified notes provided by the user, which may be incomplete or inaccurate and could affect the result.

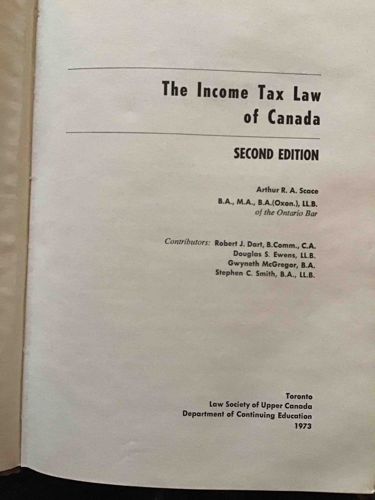

This item is a legal textbook titled "The Income Tax Law of Canada," specifically identified as the "SECOND EDITION," published in 1973. The visible image displays the title page of the book, which is crafted from off-white or cream-colored paper, exhibiting the expected natural aging and slight yellowing consistent with its date of publication. The text is meticulously printed in black ink using a classic, legible serif typeface, indicative of the professional printing standards for academic and legal publications of the mid-20th century. The principal author is Arthur R. A. Scace, with additional contributors including Robert J. Dart, Douglas S. Ewens, Gwyneth McGregor, and Stephen C. Smith; all are noted with their respective academic and professional credentials. The publisher is clearly stated as the Law Society of Upper Canada, Department of Continuing Education, located in Toronto, which signifies its authoritative nature and targeted audience of legal practitioners in Canada. The overall condition is stated as "Good condition," suggesting that despite its age, the book has been well-preserved, showing no significant tears, heavy creasing, or major staining visible on the title page. The binding, though not fully visible, appears to be a standard, sturdy form for a legal treatise, enabling reliable use. Its role as a second edition indicates its importance as an updated and revised reference regarding Canadian income tax legislation during that era. The craftsmanship, evident in the clear typography and consistent paper quality, points to a professionally produced and durable legal resource.

AI Appraisal Report

·AI can make mistakes·Verify before acting

Having carefully examined the provided image and the description of 'The Income Tax Law of Canada, Second Edition' by Scace et al., published in 1973 by the Law Society of Upper Canada, I can provide the following appraisal.

Condition and Authenticity: Based on the image, the title page presents as authentic for a 1973 publication, displaying expected natural aging and yellowing consistent with its vintage. The text appears clear and legible. The owner states "Good condition," which, if accurate across the entire volume, suggests it is well-preserved with no major tears, creases, or staining visible on the title page. However, my assessment of authenticity is limited to the visual information available. Without physical inspection, I cannot verify the integrity of the binding, confirm completeness of all pages, assess internal foxing, damp staining, or the presence of significant annotations. A full physical examination would be necessary to confirm the overall internal condition and binding health.

Market Conditions and Value Factors: This item falls into the category of an outdated legal textbook. While historically relevant for Canadian legal studies, the content itself is obsolete, significantly limiting its demand among legal professionals who require current legislation. Its primary value is to specialized collectors of Canadian legal history, specific institutional libraries, or individuals with a personal connection to the authors or the Law Society of Upper Canada.

Demand and Rarity: Demand for such specific, out-of-date legal treatises is generally low. While not mass-market, it's not considered rare within the broader antique book market. Second editions, by their nature, are less unique than scarce first editions or those with significant provenance (e.g., author's copy, famous lawyer's library copy).

Appraisal: Considering the factors above, including its "Good condition" for a book of its age, but offset by its niche market and obsolete content, I appraise 'The Income Tax Law of Canada, Second Edition' to be valued between $25 and $75 CDN. This reflects its modest historical interest rather than any significant market rarity or functional value.